Introduction

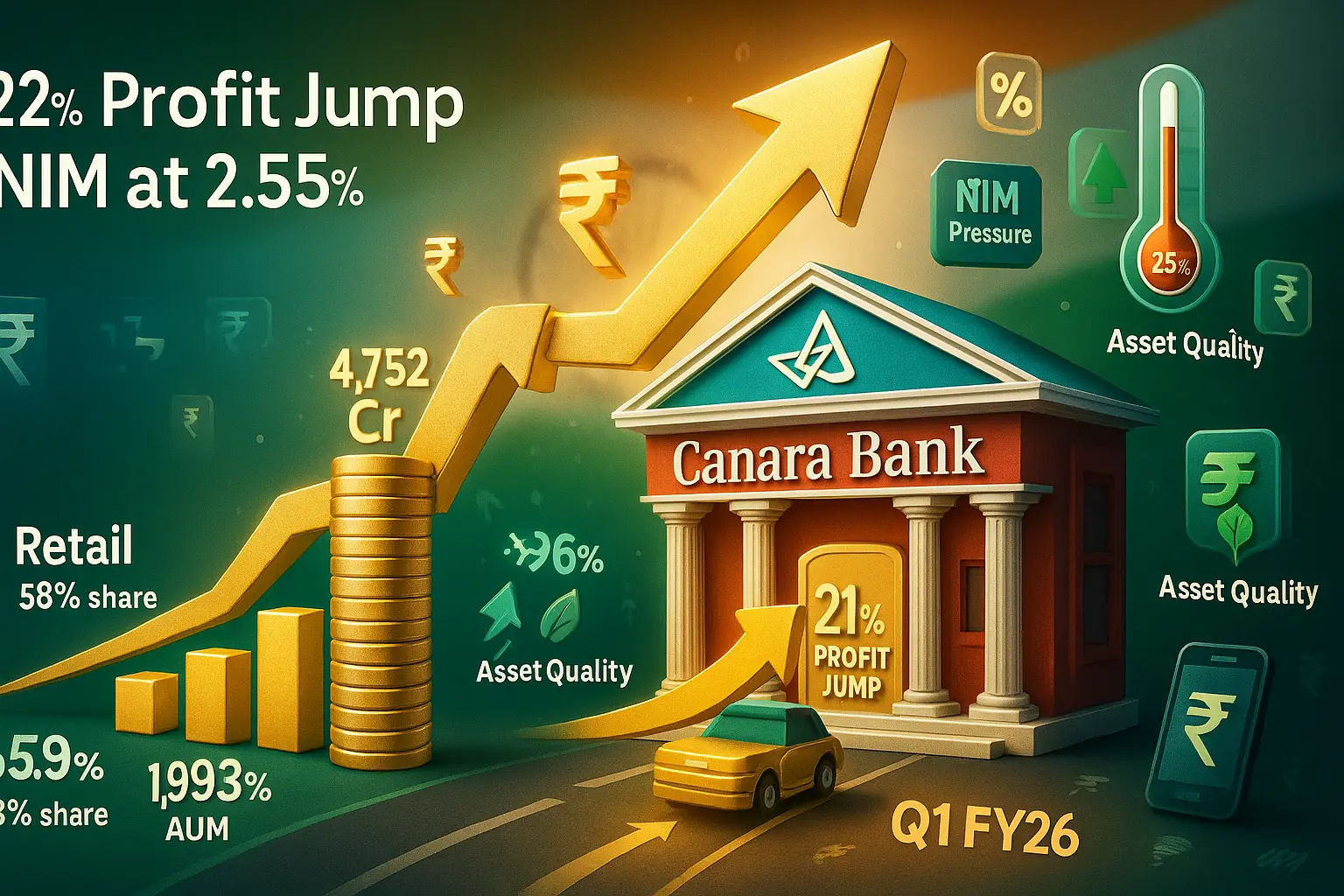

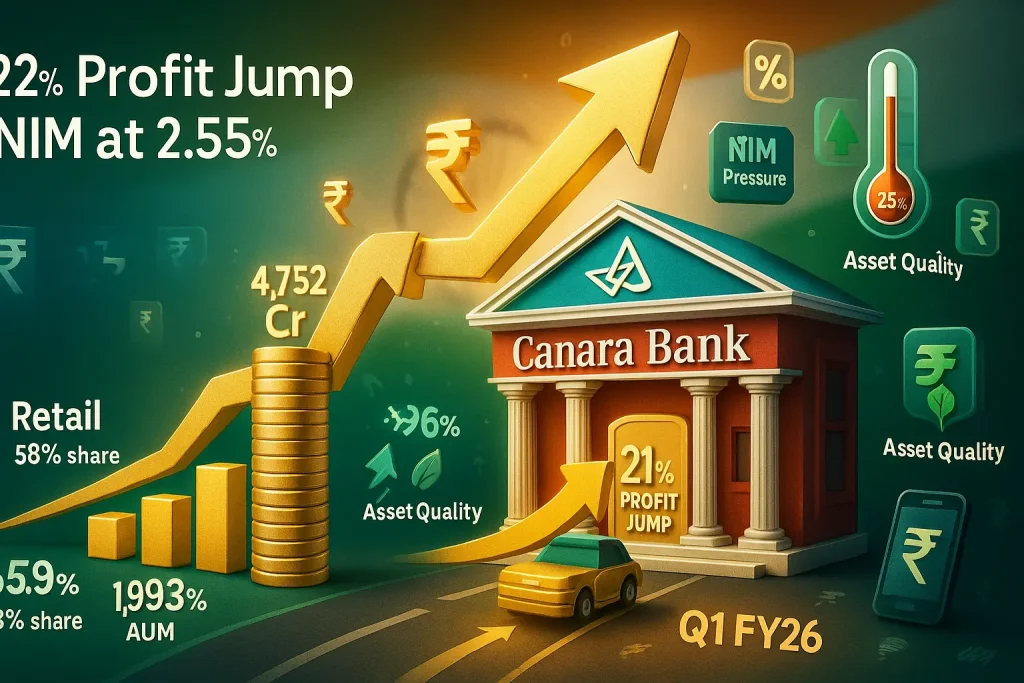

Canara Bank, one of India’s leading public sector banks, reported a 21.7% YoY jump in net profit to ₹4,752 crore in Q1 FY26 (April–June 2025), driven by strong treasury gains and fee income despite a marginal decline in net interest income (NII). The bank’s asset quality continued to improve, with gross NPAs falling to 2.69%, while retail and MSME loans saw robust growth.

This detailed analysis covers:

✅ Financial highlights & key metrics

✅ Segment-wise performance (RAM, corporate loans, deposits)

✅ Asset quality & provisioning trends

✅ Management commentary & future outlook

✅ Market reaction & investor takeaways

Key Financial Highlights

| Metric | Q1 FY26 | Q1 FY25 | Change (YoY) |

|---|---|---|---|

| Net Profit (PAT) | ₹4,752 Cr | ₹3,905 Cr | +21.7% |

| Net Interest Income (NII) | ₹9,009 Cr | ₹9,166 Cr | -1.7% |

| Other Income | ₹7,060 Cr | ₹5,319 Cr | +32.7% |

| Operating Profit (PPOP) | ₹8,554 Cr | ₹7,616 Cr | +12.3% |

| Global Advances | ₹10.96 Lakh Cr | ₹9.75 Lakh Cr | +12.4% |

| Global Deposits | ₹14.68 Lakh Cr | ₹13.35 Lakh Cr | +9.9% |

Key Observations:

- Profit Growth: Driven by a 296% YoY surge in treasury income (₹1,993 Cr) and 16% rise in fee income (₹2,223 Cr) .

- NII Decline: Due to higher deposit costs and RBI’s repo rate cuts impacting lending yields .

- Credit Growth: Retail loans surged 33.9%, while RAM (Retail, Agri, MSME) loans grew 14.9% .

Segment-Wise Performance Breakdown

1. Loan Growth & Business Expansion

- Retail Loans: +33.9% YoY (Housing loans +13.9%, Vehicle loans +22.1%) .

- RAM Portfolio: 58% of total loans, growing at 14.9% YoY .

- Corporate Loans: Modest growth, maintaining a 42% share of the loan book .

2. Deposit Trends

- CASA Growth: +3.7% YoY (₹3.95 Lakh Cr), but current account deposits fell 30% QoQ due to PSU withdrawals .

- Term Deposits: +11% YoY, reflecting higher interest rates attracting fixed deposits .

3. Treasury & Fee Income

- Treasury Gains: ₹1,993 Cr (vs. ₹503 Cr YoY) due to bond sales .

- Fee Income: ₹2,223 Cr (+16% YoY) from cross-selling and bancassurance .

Asset Quality & Risk Management

| Parameter | Q1 FY26 | Q1 FY25 | Improvement |

|---|---|---|---|

| Gross NPA (%) | 2.69% | 4.14% | -145 bps |

| Net NPA (%) | 0.63% | 1.24% | -61 bps |

| Provision Coverage Ratio (PCR) | 93.17% | 89.22% | +395 bps |

Key Developments:

- Slippages Declined: Fresh slippages at ₹2,129 Cr (vs. ₹2,655 Cr in Q4 FY25) .

- Recoveries & Upgrades: ₹1,414 Cr from written-off accounts .

- Credit Cost: Improved to 0.72% (from 0.90% YoY) .

Management Commentary & Future Outlook

1. NIM Pressure & Deposit Rate Cuts

- NIM at 2.55% (vs. 2.9% YoY) due to RBI’s 100 bps repo rate cut .

- MD & CEO K Satyanarayana Raju stated:

- “Deposit rates were cut by 50+ bps in June; cost of funds will decline in Q2” .

- “We expect NIM to stabilize at 2.6–2.7% in FY26” .

2. Growth Strategy

- Focus on RAM loans (targeting 15% YoY growth) .

- Digital Push: Expanding mobile banking and UPI-based services .

3. Asset Quality Guidance

- Gross NPA target: Below 2.5% by FY26-end .

- Slippage ratio: To remain <1% .

Market Reaction & Investor Takeaways

1. Stock Performance

- Post-Results Rally: Shares surged 5.3% to ₹113.50 on BSE .

- YTD Return: +13% (outperforming Nifty PSU Bank Index) .

2. Analyst Views

- Bullish: Strong fee income, improving asset quality .

- Cautious: NIM compression and deposit cost pressures .

3. Investment Strategy

✅ Short-Term Traders: Buy on dips (support at ₹108–₹110).

✅ Long-Term Investors: Accumulate for dividend yield (3.5%) and RAM growth.

⚠️ Risks: Further rate cuts, slower deposit growth.

Conclusion: A Balanced Quarter

Canara Bank’s Q1 FY26 results reflect strong profitability and asset quality improvement, though NIM pressures persist. Investors should monitor:

🔹 Deposit repricing impact in Q2

🔹 Retail/MSME loan growth sustainability

🔹 RBI’s monetary policy stance

Disclaimer: Not investment advice. Consult a SEBI-registered advisor.

What’s your view on Canara Bank’s results? Share in comments! 💬